This article from Shelterforce Magazine outlines the growing trend of municipal sponsorship of Community Land Trusts including profiles of new CLTs in Irvine, CA and Chicago.

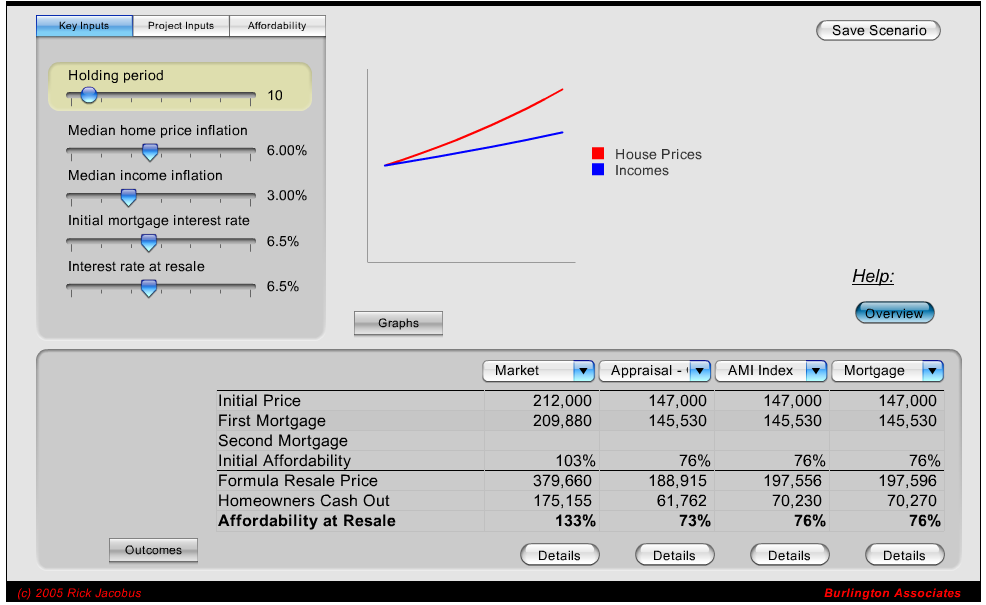

This general purpose educational tool was designed to help community leaders understand the relative performance of different limited equity resale formulas. So much of what sets one model apart from the other is dependant on the assumptions you make about interest rates, home price inflation and income growth. This tool allows a side-by-side comparison between several models, and allows you to change these input assumptions and immediately see changes in the relative performance of each of the models in terms of both ongoing affordability and equity building for homeowners. The tool also allows you to look up historical data on home prices and median incomes for every metropolitan area in the country in order to get a better feel for what appropriate assumptions might be going forward.

The tool compares several of the most common resale formulas including a basic AMI index, an appraisal based formula, a mortgage based formula and a shared equity loan model.

The tool is intended to help policy makers to evaluate questions like:

· When housing costs are rising rapidly, which approach preserves affordability best?

· Which approach provides the greatest asset building opportunity in the face of rising interest rates?

· If incomes grow more slowly than we expect, which approaches will be most impacted?

You can make the analysis more relevant to your local conditions by customizing a number of background assumptions like cost of production for a new affordable unit, the level of subsidy available, and the monthly housing costs that homeowners will face.

In recognition of the significant benefits of homeownership for families and the communities in which they live, many cities, counties and states have adopted policies that seek to increase residents’ access to affordable homeownership opportunities. This paper examines the range of different policy options that communities have adopted to reduce the cost of homeownership, with a particular focus on the effectiveness of each option in preserving affordable homeownership opportunities over time.

The focus of this review on the preservation of affordable homeownership grows out of the collective experience of numerous communities around the country with sharply rising home prices over the past five to ten years. As many communities have learned the hard way, homes that they helped make affordable through an initial downpayment grant or other assistance often have become unaffordable when sold to the next family. With the amount of subsidy needed to bring homeownership within reach of working families growing exponentially, communities have struggled with the question of how to ensure that the public’s investments in homeownership keep pace with the market. This review provides an overview of the range of mechanisms that local governments use to ensure that housing funds invested in affordable homeownership today are able to serve additional families into the future. In general, this is accomplished either through resale restrictions that preserve the affordability of specific assisted units or through deferred loans that allow the locality to capture a portion of home price appreciation at the time that assisted units are sold that can then be used to help subsequent buyers purchase homes of their choice.

Download Shared Equity, Transformative WealthWritten by Rick Jacobus.

Published by the Center for Housing Policy of the National Housing Conference.

This paper provides an analysis of several alternative strategies for sharing the equity growth that accompanies home price appreciation to balance the dual goals of individual asset accumulation and ongoing affordability to future home purchasers.

As home prices have risen over the past decade, many local government homeownership programs have been forced to dramatically increase the level of public subsidy available to each family – some are now providing well over $100,000 per family. As subsidy levels have risen, more and more jurisdictions have turned to shared equity approaches that split the equity that results from home price appreciation. Under these approaches, a portion of the equity growth goes to the homeowner – augmenting the asset growth they achieve through paydown of principal on their mortgage – and a portion either stays attached to the home to ensure its ongoing affordability or goes back to the local government to be used to help subsequent purchasers afford to buy a home.

Despite their great benefits, shared equity approaches are sometimes criticized from an asset-building perspective because they prevent homeowners from realizing the full wealth-creation benefits associated with traditional homeownership. In The Hidden Cost of Being African American, Thomas Shapiro uses the term “Transformative Assets” to refer to assets like homeownership that transform people’s lives and lead to better lives for their children. It is clear that traditional homeownership can have this kind of impact – at least in a stable or rising housing market – but what about shared equity homeownership? Given all the controversy over shared equity homeownership, it seems worth asking: how do shared equity homeownership programs perform as asset-building mechanisms? How do the returns available in these programs compare with market-rate ownership? Do some shared equity approaches do a better job of generating meaningful wealth while still preserving affordability? Is the equity that shared equity homeowners earn enough to change people’s lives?

in California Affordable Housing Deskbook, Solano Press.

Written for local elected officials and housing program administrators, this chapter explains how Community Land Trusts operate and places them within a continuum of other policy alternatives.

I created this interactive tutorial on the economics of permanently affordable housing after trying to explain these concepts to small groups with static PowerPoint slides. The key to understanding the growing homeownership affordability challenge is the relative rates of change of housing prices and incomes. I found that this idea was difficult to explain verbally but was easy for people to understand with the help of simple drawings. To create the tutorial, I had to not only create the images and write the accompanying text but build a complex user interface to allow people to control the flow of the presentation and skip forward and backwards.

The presentation has proven extremely popular and has been shown by myself and a number of other advocates to thousands of people at a series of housing and urban development conferences. The latest version includes an imbedded voice narration. The presentation can also be run without the audio with either full text narration on screen or with bulleted text for live presentations to groups.

There are real neighborhood differences in the rate at which home mortgages were resold on the secondary market.

There is no doubt that information technology has brought about huge changes in world financial markets. Markets which used to be largely isolated are now inextricably interconnected by a real time network of transactions in which, generally, capital flows instantly to the highest bidder regardless of the location of that bidder on the globe. We might expect this trend, which Richard O’Brian calls this “the end of geography,” to be good news for low-income communities. One could conclude that the development of an integrated and standardized financial network, by reducing the role of potentially biased individual lenders, could reduce racial and income discrimination and move the economy toward a situation where capital is allocated based entirely on the real value which various sectors contribute. And yet low-income urban communities in America and elsewhere appear to be experiencing increasing capital shortages.

This paper identifies an emerging structural logic of the financial system under which investment decisions are made by a network that relies on previous transactions as the main source for information about credit quality. The home mortgage market in the United States is examined as a specific case of this more general global financial market transformation. Data relating to the secondary market for single family home mortgages in the Oakland, CA metropolitan area is employed to provide empirical support for the argument that the emerging financial network itself has distinct geographic preferences which place low-income and minority neighborhoods at a systematic disadvantage in the competition for capital.

You must be logged in to post a comment.